Ever since the Goods and Services Tax (GST) Bill was passed in the Parliament, it has created widespread confusion and speculation in the market as to how its introduction would impact each of us.

With the implementation of GST on July 1, 2017, there has been major tax implications across all financial and economic sectors. But, do you know what GST actually is and how it affects the insurance sector?

So what is GST?

The Goods and Service Tax is a unified tax system which removed the multiple taxes charged on a good or a service. GST is one of the most important tax reforms ever introduced in India. GST is charged on the manufacture of goods and delivery of services.

Insurance and GST

Insurance, being a part of the financial sector, has also been affected by GST. There are four tax slabs under the GST regime which are 5%, 12%, 18% and 28% and insurance, being a service industry, is taxed at 18%.

Impact of GST on insurance

GST imposition has raised the tax component in the premium of an insurance policy. Earlier, a service tax of 15% was charged on the premium which has increased to 18% under the new GST regime. However, different types of insurance plans have been affected differently. Let’s understand how:

- Life insurance

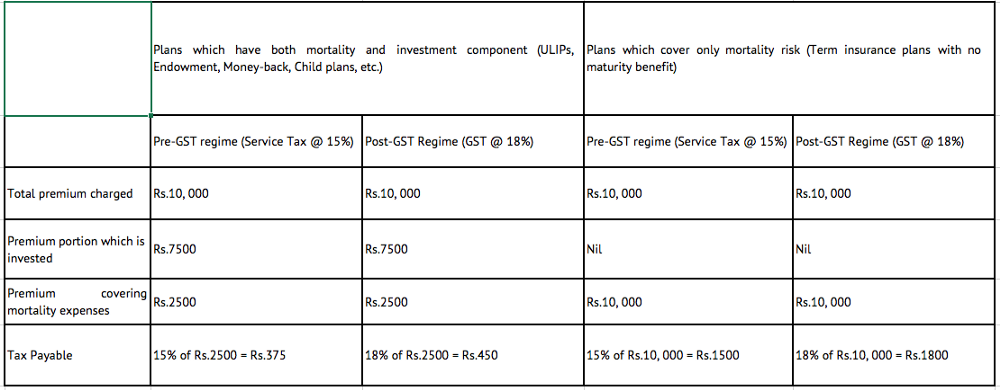

In case of life insurance policies, the premium is broadly composed of two parts — i) the cost of insuring the mortality risk & ii) the investment made by the insurance company which yields the maturity benefit.

Tax is levied on that portion of the premium which represents the cost of mortality. Therefore, different life insurance plans have different tax incidence. For instance in case of term plans where there is no maturity benefit the entire premium represents cost of mortality. Thus, tax is levied on the entire amount of premium. Due to GST, the premiums of term plans are, thus, expected to increase by 3%. In case of endowment plans, tax increase of 3% would be applicable only on the premium which is the cost of mortality. Thus, there is not much increase in premium as the mortality cost is low. Similarly, in ULIP plans, majority of the premium is meant for investments and only a fraction of it is deducted for mortality cost. For ULIPs too, therefore, premium increase would be marginal.

Let us understand with the help of example:

However, if you opt for Government-backed insurance schemes like Janashree Bima Yojana (JBY), Aam Aadmi Bima Yojana (AABY), etc. there would be no impact of GST.

- Health insurance

Health insurance policies would see a rise in the premium rate. Against the earlier applicable 15% service tax, you would have to pay 18% on the GST imposed on health insurance plans

- Motor insurance plans

Motor insurance plans would also become dearer as there would be a tax increase of 3% on the overall premium. Whether you buy a comprehensive or a third-party motor insurance policy for your bike or your car, be prepared to shell out more.

- Travel insurance plans

The same story goes for travel insurance plans. A GST of 18% is charged on the premiums which increases your outgo by 3%.

What can you, as an investor expect?

By now you must have understood that for any form of insurance you would have to loosen your purse strings a little more than before. However, don’t be deterred. The premiums would increase by only 3% on the tax rate — a marginally higher premium against the benefits promised by various types of insurance plans.

Say, for instance, a health insurance policy of Rs.5 lakh covering yourself, your spouse and your children, was available at a premium of Rs.10,000. Under the old tax system, you would have to part with Rs.10,000 as the premium cost and 15% service tax, which brought your total expenditure to Rs.11,500. With 15% service tax being replaced by 18% GST, your total spend would now amount to Rs.11,800 — ie. an increase of Rs. 300.

Is the change that drastic and unaffordable? — When it comes to securing yourself with insurance… not really!

Consider the Rs.5 lakh coverage for the whole family. Imagine having no coverage at all. Would you be able to afford the huge financial loss you would suffer in an emergency? That too with GST added on to possibly exorbitant unexpected costs…. you’d rather secure yourself with an insurance policy upfront.

GST has changed the face of the Indian economy. Naturally, the insurance sector has also been affected. GST has increased the tax incidence, making insurance policies a tad bit more expensive. However, the benefits remain unchanged and justify the slight increase in premium.

Read more about 5 ways to boost insurance sales