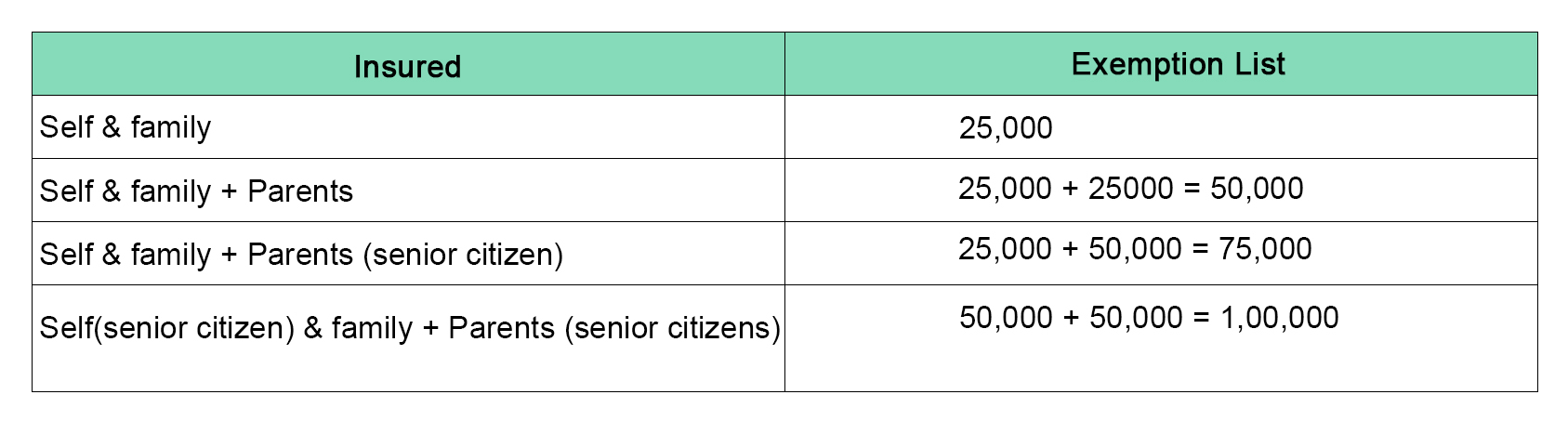

It is profoundly known that a health insurance policy can be of great worth when it comes to saving tax in accordance with the Income Tax Act. In India, the maximum limit of the deduction is Rs. 25,000/-. Now, there are cases where due to lack of knowledge regarding the provisions of tax laws, people end-up not claiming tax benefits. If you’re an insurance agent and looking forward to selling health insurances in a better way, we’ve got you covered. It is of utmost importance to claim the tax deductions in an appropriate manner. If your client’s claim is incorrect, he/she might land up in trouble for a tax scrutiny. So, let’s know about the main reasons where you could lose the tax benefits on a health insurance, try to avoid these mistakes whenever you can.

1. Paying Premium for Others:

When we talk about India, in accordance with the Section 80-D, you can only claim a deduction for the premium paid for the permitted relationships. However, there are several health insurance policies out there that allow you to cover in-laws, grandchildren, siblings and more. But, for the purpose of claiming tax deductions, you can only do that for the relationships such as Spouse, Self, Dependent children and Parents. One should know that parents can be dependent or independent, but, children should be dependent only if you’re looking forward to claiming the deduction.

In general terms, the premium paid for relationships other than the permitted ones is counted under the no tax benefit category. Hence, you should not make this mistake and should not file deductions for the same. For example, a working son who is independent can consider paying a premium for himself and his parents & not vice-versa. Thus, the legitimate tax deduction will be possible and it’ll further reduce the son’s tax liability.

2. Not Claiming the Expenses:

There might be a case where an individual didn’t produce the certificate for paying the premium to his employer. Now, in that scenario, more TDS might be deducted from one’s salary and the person will not be eligible for deductions under the section 80-D. Here comes a lifeline by the tax department, if a person pays his/her premium by the March 31st, he or she can claim it in the income tax return. An individual will receive a full refund of the extra TDS deducted by the employer in lieu of the absence of a certificate. But, people generally don’t know about this and they also don’t claim the refund in their tax returns as well. In that scenario, you can advise the customers to revise their tax returns.

3. Not Renewing the Policy:

It is an obvious fact that one can only claim the tax benefit when the policy is in an active state. Also, in a majority of cases in India and around the world, people tend to pay for the insurance premium once they receive a renewal notice or notification from the respective health insurance company. An agent must know that these renewal notices are being sent as a matter of courtesy by companies and they can stop sending the notices without any prior intimation. It is the sole responsibility of a policyholder to renew the policy on time. Failing to pay the premium is one of the prime reasons for families to lose the tax benefits on their health insurances.

4. Paying the Premium For More Than a Year:

Health Insurance agents generally know that the section 80-D comes with a unique feature which allows the policyholder to claim the respective deductions on an annual payment basis. If a policyholder is having a yearly premium of Rs. 15,000/- and he pays a combined Rs. 30,000/- for two years, the total sum will not be eligible for the tax deduction. For every year the maximum claim balance deduction stands at Rs. 25,000, hence, a policyholder should do the required math and deposit the premiums accordingly every year. Companies often tend to give discounts to people who make combined premium payments, this should not be the approach.

Although it’s perfectly legal to pay the premiums in cash, in that scenario you will not be able to claim tax benefits. If an individual is paying his or her premiums through card, net-banking or any other payment mode other than cash, he or she is eligible for a tax deduction. Health insurance policy not only protects you but it is also a tool for saving tax. One should remain aware of all the mandatory provisions and set of rules so that you never end-up losing your tax benefits.

Read more about what is PPN rate in health insurance

Read more about 5 lesser know facts about buying health insurance

Read more about how to choose a health insurance plan?

Read more about anatomy of a health insurance plan