Once people get a job their financial responsibilities start building up. They marry, have children and then plan for their family’s secure financial future. This financial planning is often considered to be a stressful thing to do because many individuals are unsure about the right investment avenues which would fulfill their financial goals. What they oversee is the fact that if the financial goals are planned considering their different life stages, they would be able to create a complete financial plan which would help them achieve their financial goals. You, as a financial advisor, should help your clients plan for their finances based on their life stage and then sell them insurance plan which would suit them. This is called life-stage selling. Are you aware of it?

Life-stage selling is a technique which always works in your favor and helps you sell. So, let’s understand this technique and the different stages of your clients’ life–

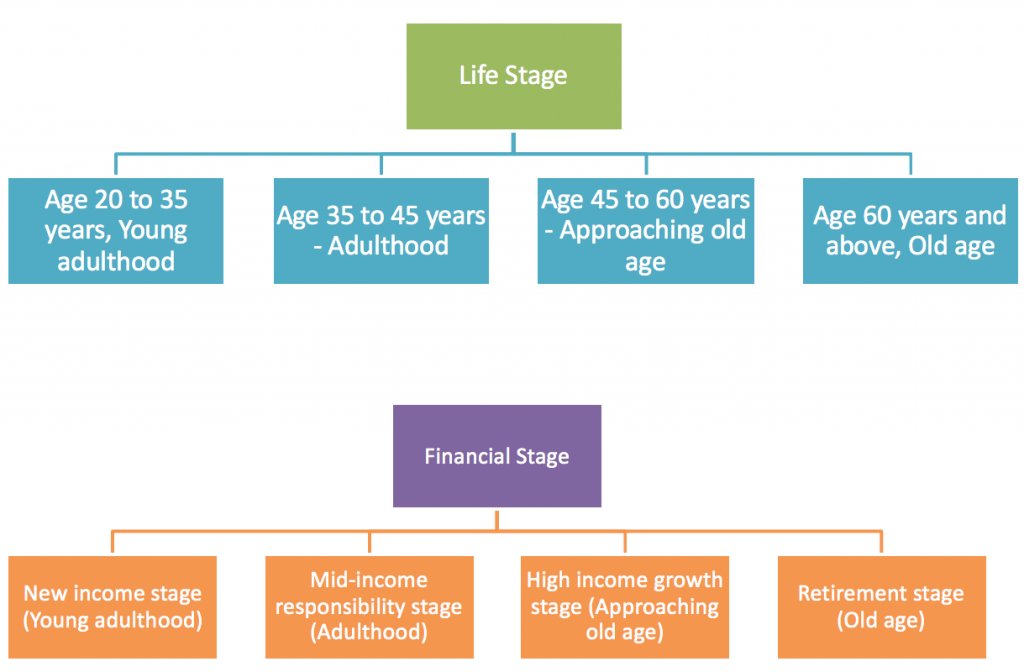

Stages in your client’s life

There are four life stages in every individual’s life and corresponding to each stage there is a financial stage. Here are the four life stages and financial stages common to your clients –

Insurance and stages of an individual’s life

Insurance needs of your clients vary at all life and financial stages. Therefore, it is essential for you to understand which stage your client is in and which insurance product would suit his/her needs. Knowledge of these stages would help you pitch the right product which, in turn, would increase the probability of sale. So, let’s understand which insurance product suits your clients at which stage–

-

Age 20-35 years, young adulthood, new income stage

At this stage, your client has just attained financial independence and is trying to build a stable career. This financial stage represents low to mid-income levels. The financial responsibilities of your clients would be low because they might not be married and even if they are, they might not have kids. Even the disposable income would be average as their earnings would most likely be spent in meeting the household and lifestyle expenses.

Suitable products–

- Term insurance is a must. This should be sufficient to cover for possible financial losses. The premium would be low, given the low age, and affordable.

- Health insurance is also necessary to cover for any unforeseen medical emergency. The plan should also have a maternity benefit if the client is married and would be starting a family soon because maternity cover comes with a waiting period.

Investment tips-

- Advice your clients to avoid too many loans as it would lead them to a debt trap.

- Majority of the savings and disposable income should be invested for future goals

- If possible, a small amount should also be contributed towards retirement planning to build a substantial corpus in future

-

Age 35-45 years, adulthood, mid-income responsibility stage

When your clients cross 35 years of age, they are considered to be adult and matured. Their financial priorities change as do their incomes. Since they have gained good experience at this stage their income ranges from medium to high. However, they have very high responsibilities too. They have to plan for their children’s financial future, pay for their children’s education, take care of their aging parents, etc. As such, their disposable income is low.

Suitable products–

- The term insurance cover should be increased to reflect the increased financial worth of the individual.

- Health cover should also be high.

- A child plan is suitable to create a secured financial corpus for the child

- Pension plans with a long tenure should be considered to start building a retirement corpus

- If the client has a vehicle, motor insurance policies are mandatory

Investment tips

- The loans which have been taken should be properly managed to avoid repayment defaults

- Credit card debts should be avoided

-

Age 45-60 years, approaching old age, high-income growth stage

At this age, your clients would be in the prime of their careers. They would have low responsibilities as their children must have grown up. Existing loans would also have been paid off and, if not, the installments would be low. As such, they would have a high disposable income with which they would try and create financial assets for their family.

Suitable products–

- Deferred pension plan to contribute actively towards a retirement corpus

- An endowment or unit linked plan for creating wealth and savings

- Critical illness plan along with health insurance since the age is prone to critical illnesses

- Home insurance policy for protecting the home against contingencies

Investment tips

- Retirement planning is a must as retirement is fast approaching

- Tax planning should be undertaken to reduce tax liability

- Investments should have a long-term horizon

-

Age 60 years onwards, retirement stage, mid to low income stage

Most of your clients in this stage must have retired or facing retirement. Their financial responsibilities are nil. They just need to provide for themselves and their spouses. The disposable income would be low.

Suitable products–

- Immediate annuity plans for regular pension income

- Adequate health insurance cover for meeting frequent medical needs

Investment tips

- Existing investments should be properly managed to create a source of income

- A nominee should be appointed for all financial savings

The life-stage selling technique is a good weapon at your disposal to increase your sales. Understand the different stages and the financial needs at each stage to relate to the financial needs of your clients and sell them a suitable policy. You would not only enjoy increased sales, but you would also gain your clients’ trust.

You may also read importance of retirement planning in every stage of financial planning and learn how to guide your customers the ideal way to secure themselves when they retire.